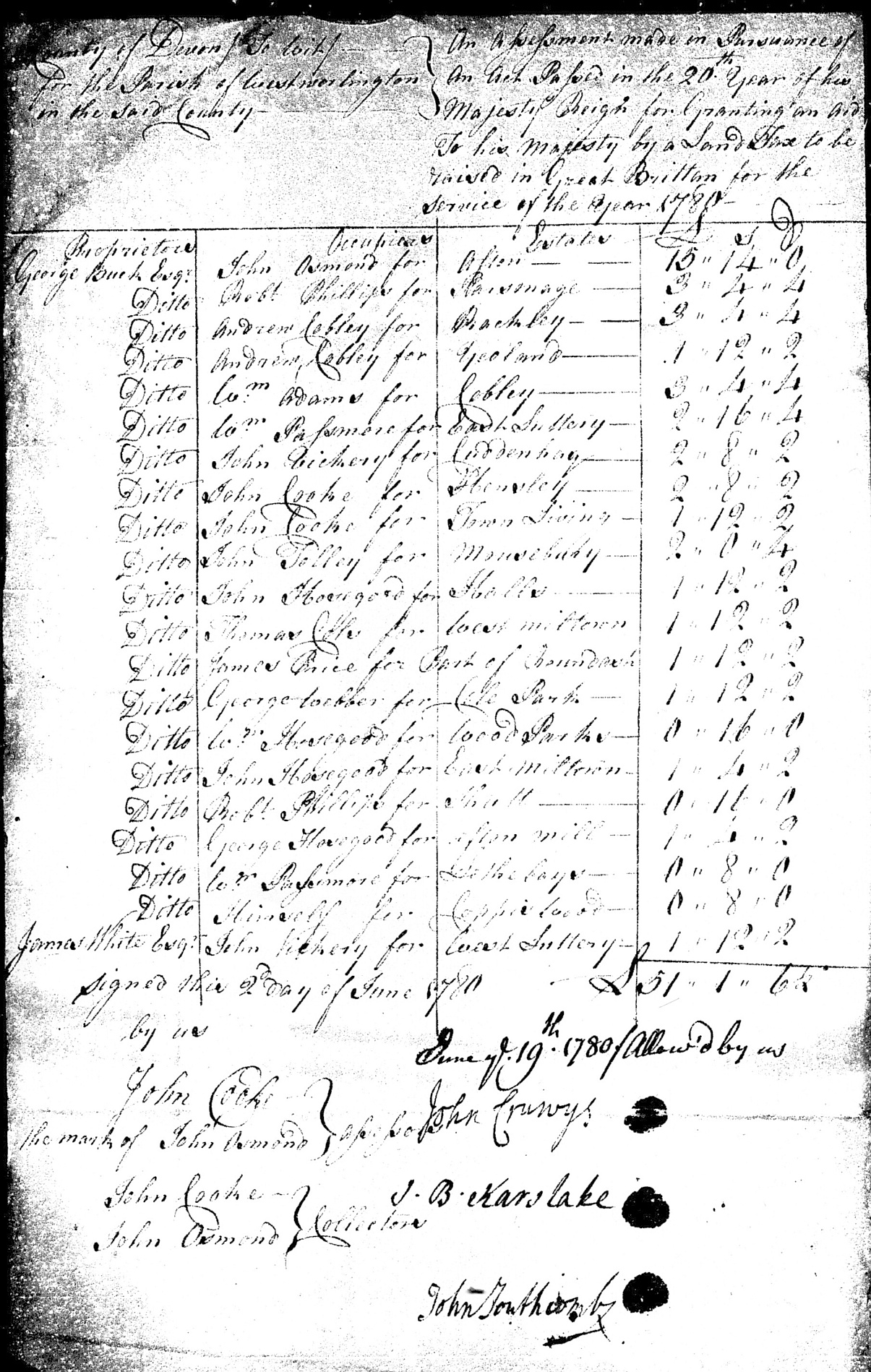

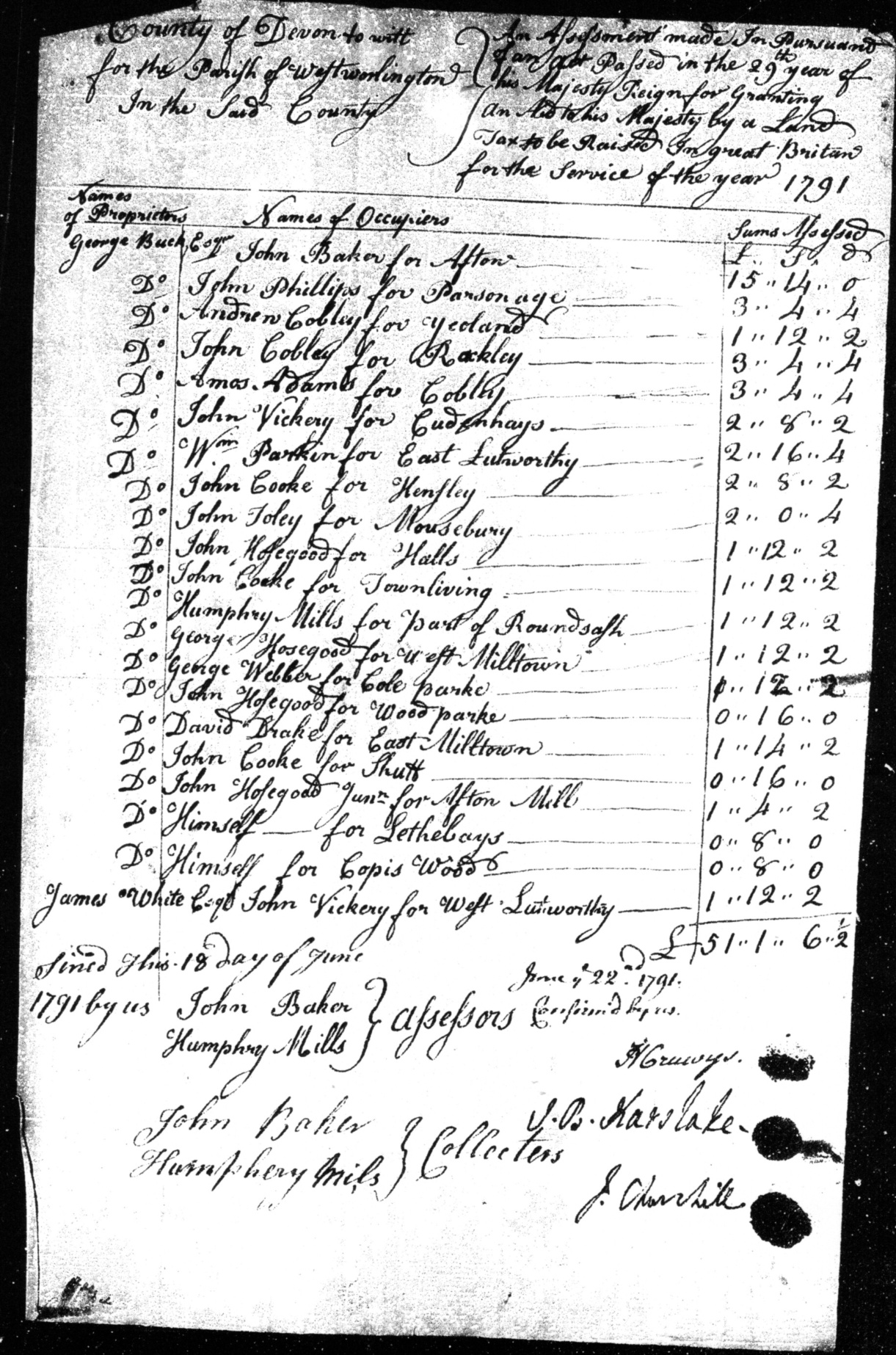

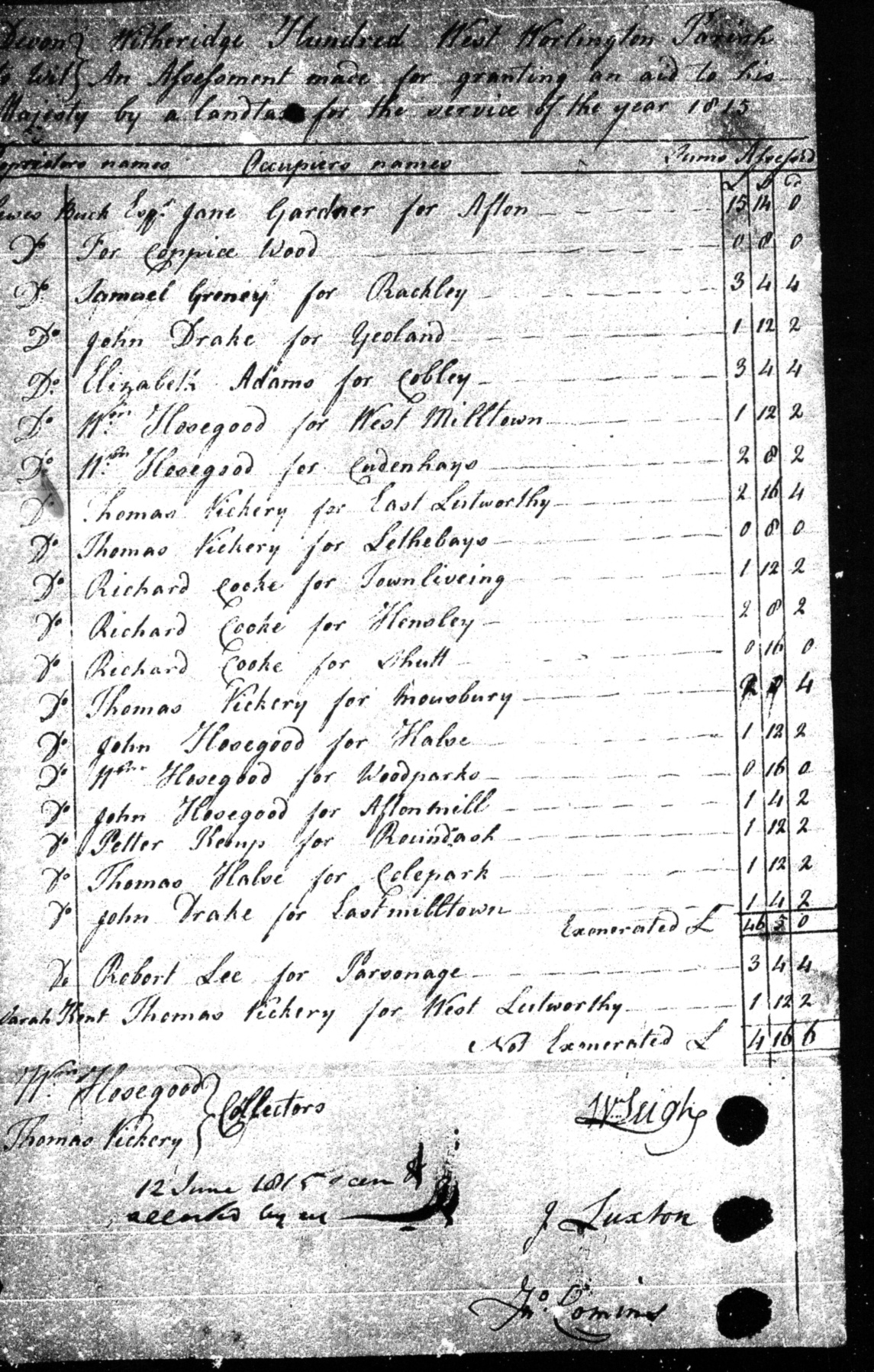

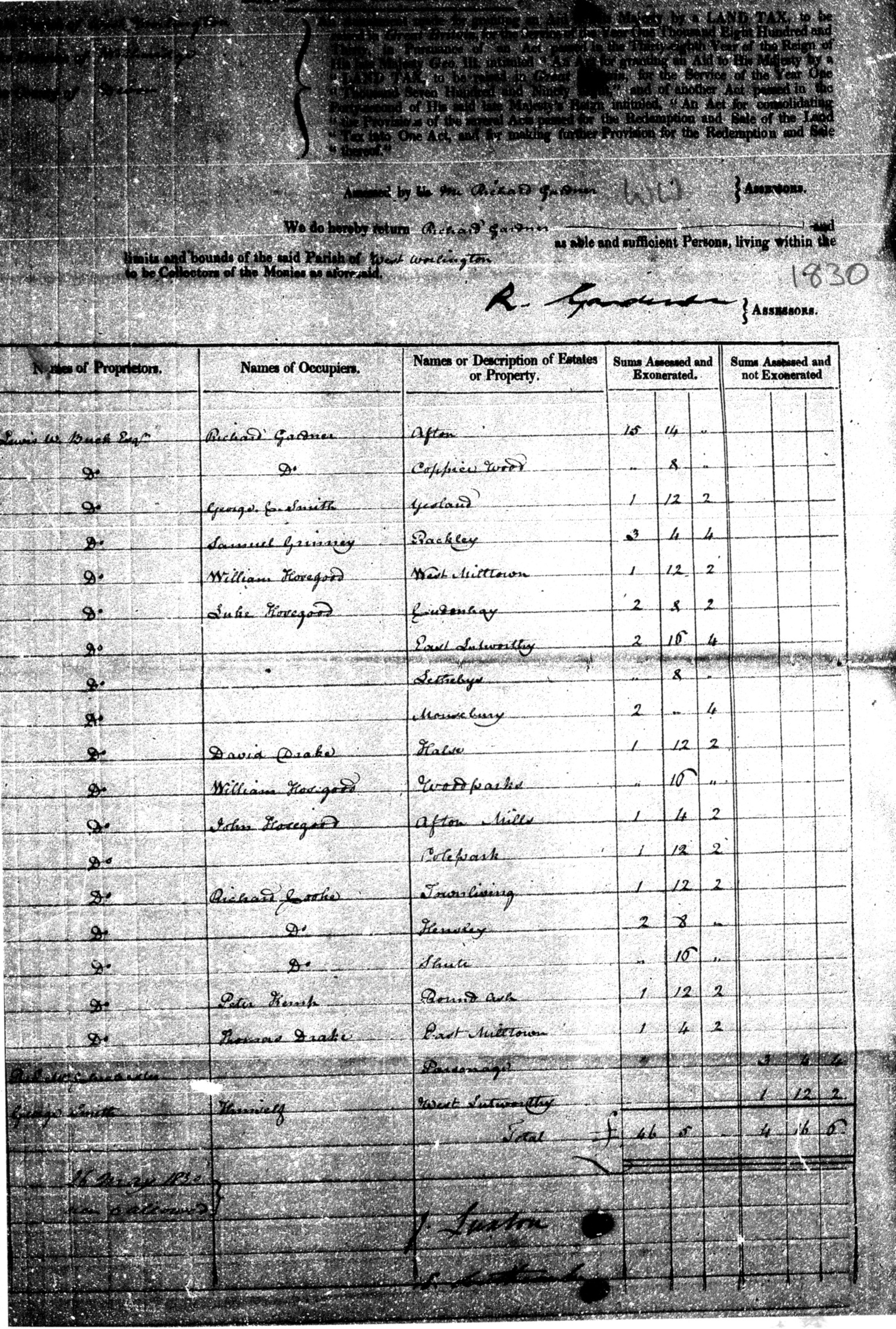

The 18th-Century Land Tax was the principal source of government revenue in the 18th century, alongside indirect taxes (excise and customs duties on consumables like salt, soap, and beer). Initially, the tax was on real estate and personal property, but from the 1730s, it was levied mainly on land and buildings, including business premises.

Parliament set the tax rate each year through a Land Tax Act, typically between one shilling and four shillings in the pound (5% to 20%) of the property’s annual value. It was based on fixed rental assessments made in 1692, which became increasingly outdated as property values changed unevenly across the country during the century. From 1780, paying the land tax on freehold property worth £2 or more per year was a qualification for voting, which meant the assessments were carefully recorded and preserved.

Unpaid local “commissioners” (usually gentry) were nominated by Parliament to oversee the process, using local men of “modest means” as collectors.

Land Tax assessments are important historical records, typically listing the name of the landowner, the occupier (especially after 1772), and the assessed amount.

In the following sections click on the down chevron at the right to view each document and click on the document image to view a larger version.